MLB Prop Expected Value: How to Calculate Edge Before Every Bet

Table of Contents

- Why Expected Value Separates Long-Term Winners from the Rest

- Converting Decimal Odds to Implied Probability

- Estimating True Probability Using Stats and Models

- The EV Formula: Worked Calculation for an MLB Prop

- Closing Line Value: Measuring Your Accuracy Over Time

- Common EV Mistakes: Small Samples, Biased Inputs, Ignoring Vig

- Expected Value Questions Answered

Why Expected Value Separates Long-Term Winners from the Rest

I spent my first two years betting MLB props without ever calculating expected value. I had winners. Some weeks I felt sharp. But at the end of each season, my bankroll sat roughly where it started — or slightly below. The problem was not my selections. It was that I had no framework for distinguishing a genuinely good bet from one that merely felt good. Expected value gave me that framework, and everything changed.

The numbers are stark: only 3-5% of sports bettors are profitable over the long term. The other 95% are not necessarily making bad picks — many of them identify the right side of a prop more often than not. What they lack is the discipline to bet only when the price offers value. At standard -110 pricing (the American format common on US platforms, equivalent to roughly 1.91 in decimal odds), a bettor needs a 52.38% win rate just to break even. That 2.38% above coin-flip is the vig — the operator’s cut. Every bet you place without a probability edge above that threshold is a slow donation to the sportsbook’s bottom line.

Expected value — EV — quantifies the gap between what you believe the true probability of an outcome is and what the sportsbook’s odds imply. When your estimated probability exceeds the implied probability, the bet has positive expected value (+EV). When it falls short, the bet has negative expected value (-EV). Over hundreds of bets, the sum of your EV determines your profit or loss, regardless of short-term variance. A bettor who places 300 bets with an average EV of +4% per bet will be profitable at the end of the season. A bettor who places 300 bets with an average EV of -2% per bet will not, no matter how many individual winners they celebrate along the way.

This guide walks through the full calculation, from converting odds to estimating true probability, with worked examples drawn from real MLB prop scenarios. Every step uses tools and data that are free and publicly available. You do not need expensive software or a mathematics degree — you need a system and the discipline to apply it consistently.

Converting Decimal Odds to Implied Probability

Before you can calculate EV, you need to speak the language of probability. Decimal odds — the standard format on UK sportsbooks — convert to implied probability with a single division. Take the number 1, divide it by the decimal odds, and multiply by 100. That is it.

A pitcher’s strikeout over is priced at 1.85. The implied probability is 1 divided by 1.85, which equals 0.5405, or 54.05%. The sportsbook is telling you, through its price, that this outcome has roughly a 54% chance of happening. If you believe the true probability is higher than 54%, the bet carries positive expected value. If you believe it is lower, the bet carries negative expected value. The entire EV framework rests on this comparison.

A home run anytime prop is priced at 4.00. The implied probability is 1 divided by 4.00, which equals 0.25, or 25%. If your Statcast-driven analysis tells you the hitter has a 30% chance of going deep tonight, the gap between 30% and 25% is your edge. If your analysis says 22%, you are looking at a negative-EV play despite the appealing payout.

One important nuance: implied probability derived from a single line includes the vig. The true “fair” probability is slightly lower than the implied probability because the sportsbook has inflated both sides of the market. On a two-way prop (over/under), you can estimate the vig by adding the implied probabilities of both sides — they will sum to more than 100%. The excess is the overround. For example, if the over is priced at 1.85 (implied 54.05%) and the under is priced at 2.00 (implied 50.00%), the sum is 104.05%. The overround is 4.05%, and the vig on each side is roughly half that. Adjusting for vig gives you a cleaner baseline, but for practical purposes the raw implied probability is a sufficient starting point for most EV calculations.

To remove the vig and find “fair” probabilities, divide each side’s implied probability by the total overround. The over’s fair probability becomes 54.05 divided by 104.05, which equals 51.95%. The under’s fair probability becomes 50.00 divided by 104.05, which equals 48.05%. These now sum to 100%. The difference between the raw implied probability (54.05%) and the vig-adjusted fair probability (51.95%) is the margin you are paying the sportsbook on that side. Understanding this spread helps you gauge how aggressively a book is pricing a particular prop — some markets carry a 3% overround, others push above 6%, and the larger the overround, the harder it is to find positive EV.

Fractional odds, still used by some UK books for certain markets, convert differently. Odds of 5/4 mean you win five units for every four staked. To convert to implied probability: take the denominator (4), divide by the sum of numerator and denominator (5 + 4 = 9), and multiply by 100. So 5/4 implies a 44.4% probability. I recommend working exclusively in decimal odds for MLB props — it makes the EV maths faster and less error-prone.

Estimating True Probability Using Stats and Models

This is the hard part. Converting odds is arithmetic. Estimating true probability is analysis. It is also where the entire edge lives — if your probability estimates are accurate more often than the market’s, you win money over time. If they are not, no amount of clever bet-sizing will save you.

I use a layered approach that does not require a proprietary model or a computer science degree. The first layer is the base rate. For a strikeout over/under, the base rate is the pitcher’s K/9 or per-start strikeout average over a meaningful sample — at least 10-15 starts. If a pitcher averages 7.2 strikeouts per start over his last 20 outings, that is my starting point for a line set at 6.5.

The second layer is the matchup adjustment. How does tonight’s opposing lineup strikeout rate compare to the league average? If the league average team K rate against right-handed pitching is 23% and tonight’s lineup strikes out 28% of the time against righties, the pitcher’s expected K-total shifts upward. I apply a simple multiplier: the ratio of the opposing lineup’s K-rate to the league average, applied to the pitcher’s base rate. So 7.2 multiplied by (28/23) equals approximately 8.8. That adjusted projection now sits well above the 6.5 line, suggesting the over has merit.

The third layer adds contextual variables: umpire zone size, ballpark, weather, pitch count expectations and recent form (trailing 3-4 starts versus season average). Each variable nudges the projection up or down by a fraction. No single contextual factor swings the projection by more than half a strikeout in my experience, but they compound. A generous-zone umpire plus a lineup with a high chase rate plus a pitcher on full rest can collectively push the projection up by a full strikeout compared to the base rate.

I assign rough adjustment values to each contextual factor based on historical data. A top-quartile umpire zone adds about 0.3-0.5 K to the projection. A hitter-friendly park adds 0.2-0.4 total bases to a total bases prop projection. Cold weather below 50 degrees Fahrenheit subtracts 0.3-0.5 from a home run probability estimate. These are not precise — they are informed estimates that I have calibrated over several seasons by comparing my projections to actual outcomes and adjusting the weights. The goal is not precision on any single game. It is systematic accuracy over a full season of 200-plus bets.

The fourth layer is converting the adjusted projection into a probability of clearing the line. If my projection for tonight’s start is 7.8 strikeouts and the line is set at 6.5, I need to estimate the probability that the actual result exceeds 6.5. Strikeout distributions for individual pitchers are roughly normal around their projection, with a standard deviation of about 2.0 Ks. Using that distribution, a projection of 7.8 against a line of 6.5 yields approximately a 73% probability of clearing the over. That is my true probability estimate.

Is this precise? No. It is an informed approximation, and the individual estimate for any single game will be wrong by some margin. But over 200-300 bets in a season, the systematic application of this method produces probability estimates that are more accurate than the market’s pricing more often than not — and that is all you need. Simon Noy, SVP of Trading at Kambi, noted in their 2025 trends report that the scale of their network gives them a unique vantage point on where the market is heading. Your job as a bettor is not to build a better model than Kambi. It is to find the spots where the model’s output lags behind the data you can see.

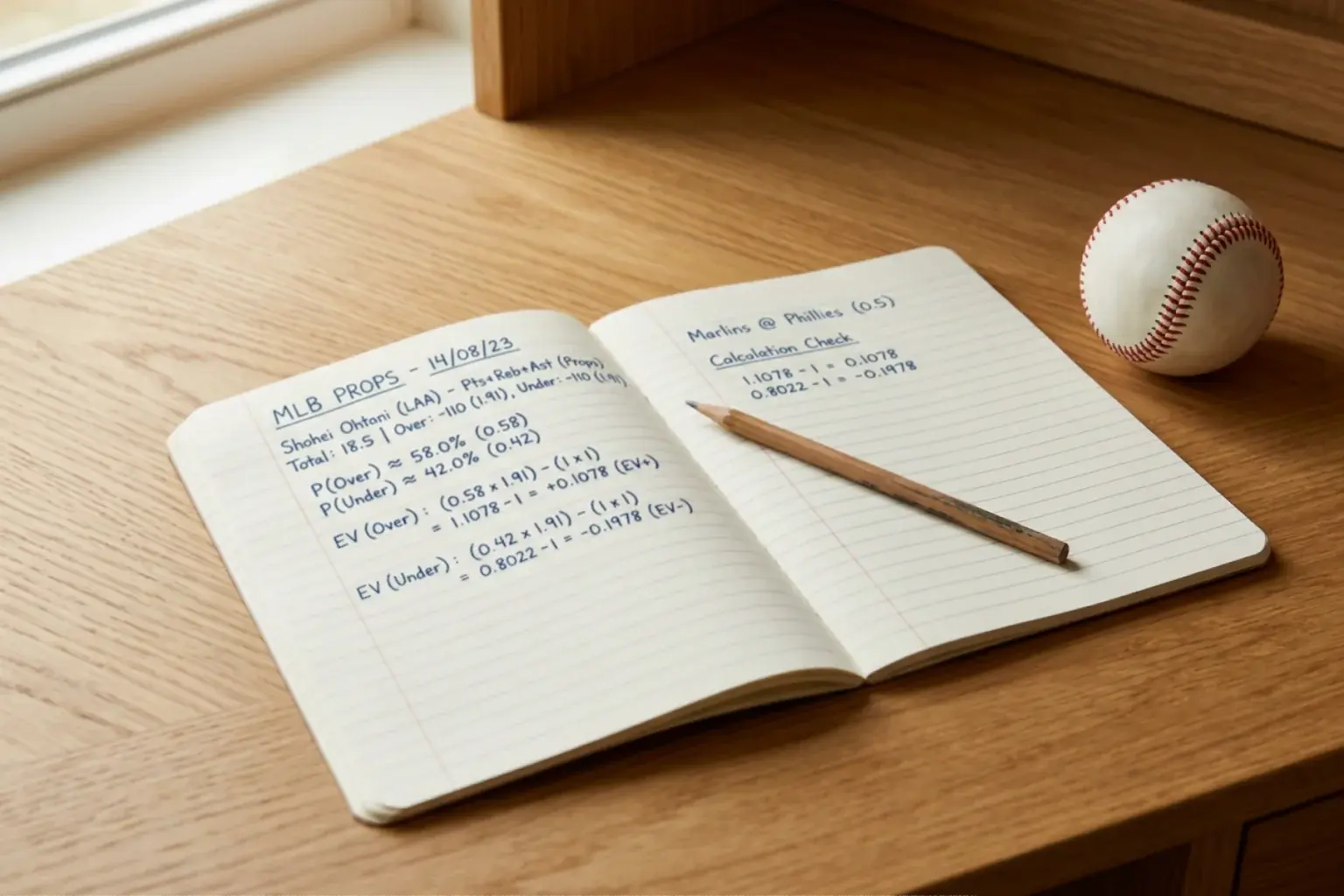

The EV Formula: Worked Calculation for an MLB Prop

Last summer I stumbled into a strikeout prop that illustrates the formula perfectly. A left-handed starter with a 12.1% swinging-strike rate was facing a lineup that struck out 29% of the time against left-handed pitching — well above the league average. The umpire assigned had a top-20% zone size. The line was set at 5.5 Ks at decimal odds of 1.80.

The EV formula is: EV = (Probability of Winning multiplied by Net Profit per Unit) minus (Probability of Losing multiplied by Stake per Unit). For a one-unit stake at decimal odds of 1.80, the net profit on a win is 0.80 units and the loss is 1.00 unit.

My estimated true probability of the over hitting was 62%. The implied probability at 1.80 is 55.6% (1 divided by 1.80). My edge: 62% minus 55.6% equals 6.4 percentage points.

Plugging into the formula: EV = (0.62 multiplied by 0.80) minus (0.38 multiplied by 1.00). That gives 0.496 minus 0.380, which equals +0.116. For every unit staked on this bet, I expected to make 0.116 units in profit over the long run. An EV of +11.6% per unit is strong — I typically require a minimum of +3% EV before placing a bet, and anything above +8% gets a higher stake.

The pitcher recorded seven strikeouts that night, clearing the 5.5 line comfortably. But the outcome of any single bet is irrelevant to the EV framework. Had he recorded four strikeouts, the bet would still have been correct given the information available. EV is a long-run metric. You are not trying to be right tonight. You are trying to be right across hundreds of nights. The gross win margin for operators sat at 9.3% in 2024, and every +EV bet you place chips away at that edge from the other side.

How do you decide what EV threshold justifies a bet? My floor is +3%. Below that, the estimation error in my probability assessment could easily wipe out the theoretical edge. Between +3% and +5%, I bet a standard unit. Between +5% and +8%, I go to 1.5 units. Above +8%, I bet two units. This tiered approach ensures that my largest positions are on the plays where my estimated edge is widest and most likely to survive real-world variance. I never exceed two units on any single MLB prop regardless of the estimated EV, because even a 15% edge means you lose 40-45% of the time. Position sizing is the guardrail that keeps a good process from being derailed by a bad week.

Closing Line Value: Measuring Your Accuracy Over Time

Closing line value — CLV — is the performance metric I wish someone had explained to me in year one. It answers a straightforward question: were the odds you got better or worse than the odds available at game time?

If you bet a K-over at 1.85 six hours before first pitch and the line closes at 1.75, you captured positive closing line value. The market moved toward your position, meaning the collective wisdom of all bettors and the sportsbook’s own adjustments confirmed that your early assessment was more accurate than the opening price. Consistently beating the closing line — even by small margins — is the single strongest indicator of long-term profitability in sports betting.

To track CLV, record the odds at which you placed each bet and the closing odds for the same market. Your CLV per bet is: (Your Odds minus Closing Odds) divided by Closing Odds. A bet placed at 1.85 that closes at 1.75 has a CLV of (1.85 minus 1.75) divided by 1.75, which equals 5.7%. Over a sample of 100-plus bets, a positive average CLV of 2-3% or higher strongly suggests your probability estimates are consistently better than the market’s.

CLV matters more than win rate for evaluating your process. A bettor with a 51% win rate and a +3% average CLV is almost certainly profitable. A bettor with a 56% win rate and a -2% average CLV is likely running above expectation and due for regression. Track both, but trust CLV as the better signal.

Tracking CLV on MLB props from the UK requires some effort because not all UK-licensed books display historical line movement or closing odds for prop markets. My workaround is simple: I record the odds at the time of my bet and then check the same market approximately 30 minutes before first pitch. That is close enough to the true closing line for practical purposes. I log everything in a spreadsheet — date, game, market, my odds, closing odds, result, and calculated CLV. After 50-60 bets, the pattern becomes visible. After 150-plus bets, it becomes statistically meaningful. If your CLV is consistently negative over a full season’s worth of bets, your probability estimates need recalibrating — not your selections, your estimates.

Common EV Mistakes: Small Samples, Biased Inputs, Ignoring Vig

Every EV calculation is only as good as the probability estimate feeding it, and there are three ways that estimate goes wrong repeatedly.

Small samples are the most common culprit. A pitcher’s K-rate over his last three starts is not a reliable input for a probability estimate. Three starts might include one blowout where he was pulled early and one rain-shortened game. The variance is enormous. I use a minimum of 10 starts for base-rate calculations and 15-20 where available. For matchup-specific data (this pitcher against this team), the sample is almost always too small to be meaningful — I rely on the broader lineup-level K-rate against the pitcher’s handedness instead.

Biased inputs are subtler. Confirmation bias — seeking data that supports a position you have already decided on — is the enemy of accurate probability estimation. If you want the over to hit because the pitcher is exciting to watch, you will unconsciously overweight the metrics that support the over and discount the ones that argue against it. I combat this by running the numbers before I form an opinion. The probability estimate comes first; the betting decision follows. If the estimate says the over is -EV, I walk away, regardless of how compelling the pitcher’s profile looks on paper.

Ignoring the vig is the third mistake, and it is surprisingly common among bettors who understand EV conceptually. The hold rate on same-game parlays runs between 20% and 35% — dramatically higher than on singles. When you build an SGP with three legs that each carry marginal +EV as singles, the compounded vig can erase the individual edges entirely. Always calculate EV on the combined ticket, not just on the legs individually. The same-game parlay strategy guide covers the compounding maths in detail.

One more thing I have learned through years of tracking my own results: your EV estimates will be wrong on individual bets. That is built into the process. What matters is systematic accuracy over hundreds of bets. If your average estimated edge per bet is +5% but your actual ROI over 300 bets is -2%, your estimates are biased upward and need recalibrating. Track your results ruthlessly, compare them to your projections, and adjust. The market is a feedback mechanism — use it.

Expected Value Questions Answered

What is a good expected value threshold to place an MLB prop bet?

I use a minimum of +3% EV before placing any MLB prop bet. Below that threshold, the edge is too thin to overcome short-term variance and potential estimation error. For single bets, +3% to +5% is a solid range that balances selectivity with volume. Above +8% represents a strong play that justifies a larger unit size. For SGPs, I require each individual leg to carry at least +3% EV independently before combining them, and I verify that the combined ticket still shows positive EV after accounting for the compounded vig.

How do you estimate true probability for a player prop without a model?

Start with the player’s base rate over a meaningful sample — at least 10-15 games or starts. Adjust for the specific matchup using the opposing team’s relevant rate against the pitcher or batter’s handedness. Layer in contextual factors: umpire zone size, ballpark, weather, recent form. Convert the adjusted projection to a probability of clearing the line using a rough distribution estimate. This layered approach does not require software or a proprietary model — it requires consistent application of publicly available data and honest probability assessment.

Does closing line movement confirm whether your MLB prop had positive EV?

Closing line value is the strongest single indicator of betting skill. If the odds at which you placed your bet are consistently better than the closing odds, the market is confirming that your early assessment was more accurate than the consensus. A positive average CLV of 2-3% or higher over 100-plus bets strongly correlates with long-term profitability. Track both the odds you got and the closing odds for every bet to measure your CLV over time.

Published by the mlb bet Props team.